Aircraft Hydraulic Pump Market to Grow 3.5%

Key Highlights

- Market growth for the global aircraft hydraulic pump market will be driven by expanding air travel, airlines increasing their fleet size, and heightened defense procurements.

- Hydraulic pumps remain critical to the operaiton of many aircraft systems, such as flilght controls and landing gears, because of their as yet unmatched power density.

- Commercial aircraft will constitute the majority of hydraulic pump installations going forward due to the large scale at which commerical aviation operates compared to other market segments.

Power architectures of aircraft are evolving gradually as electrification is introduced, efficiency margins are tightened, and digital control becomes standard across flight-critical systems. While certain mechanical interfaces are being streamlined at the aircraft level, the fundamental requirement to generate and sustain high-force, fail-tolerant actuation remains unchanged.

This is where hydraulic pumps and other hydraulic components come into play. Hydraulic pumps continue to provide the highest practical power density for converting mechanical or electrical input into the pressure required to drive flight-critical loads.

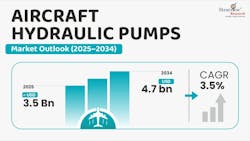

Given the continued importance of hydraulic pumps to many aircraft systems, Stratview Research is projecting the global aircraft hydraulic pump market to achieve a compound annual growth rate (CAGR) of 3.5% through 2034.

Market Drivers for Aircraft Hydraulic Pump Growth

Stratview Research’s Aircraft Hydraulic Pump Market Report cites several factors expected to drive growth for this market over the coming years. Among these is the ongoing expansion of global air travel, airlines continuing to increase their fleet sizes and heightened defense procurements in various parts of the world.

Across global aerospace markets, demand for hydraulic pumps is generated by both original equipment manufacturer (OEM) and aftermarket channels, with OEM programs accounting for the larger share.

Given North America’s concentration of aircraft manufacturers and current backlog driven delivery outlook, the region will continue to command a high share of hydraulic pump demand. The Stratview Research report notes that major OEMs such as Boeing and Lockheed Martin are in the process of ramping up production to meet increasing global commercial and defence aircraft demand.

This, coupled with high defense spending, large installed commercial and military fleets, and continuous R&D investment, are expected to keep hydraulic pump requirements structurally strong in the years to come.

A second, equally important driver for the aircraft hydraulic pump market’s future growth is fleet age. As of early 2026, commercial aircraft retirements remain near historic lows, largely due to persistent supply chain constraints and production shortfalls at major OEMs such as Boeing and Airbus. Aircraft are staying in service longer, sustaining aftermarket demand for hydraulic pumps through maintenance, repair, and replacement cycles.

Together, these structural factors support a global market valued at about USD 3.5 billion in 2025, projected to reach around USD 4.7 billion by 2034. The growth profile reflects long-term program continuity and fleet realities rather than short-term production swings.

Hydraulic Pumps: A Mature Technology with Enduring Strategic Relevance for Aircraft Systems

The concept of using hydraulics in aircraft goes back to the early 20th century when pilots sought ways to reduce manual effort in controlling larger aircraft. Before hydraulics, aircraft relied on cable and pulley systems that were heavy and required considerable force from pilots.

As aircraft became larger and faster, hydraulic systems were developed to provide greater control authority with reduced pilot workload.

A century later, hydraulic pumps remain just as mission-critical as they were at inception, and their relevance is not diminishing. Despite advances in electrification, hydraulics continue to offer unmatched power density, responsiveness, and reliability for primary flight controls, landing gears, and braking systems.

Therefore, even as the aircraft industry pushes for lighter, greener aircraft, hydraulic pumps will remain indispensable across many platforms.

The Aircraft Functions That Depend on Hydraulic Power

From landing gear and flight control surfaces to brakes and thrust reversers, hydraulic pumps turn mechanical energy into controlled, high-pressure power — a capability no other actuation technology has matched in force density and fail-safe reliability.

Hydraulic pumps are meant to be load-intensive, respond instantly and work reliably every single time.

Flight control systems alone account for two-fifths of total hydraulic pump usage, simply because ailerons, elevators, rudders, flaps, and spoilers, etc., all remain continuously active throughout every phase of flight. Unlike landing gear or thrust reversers, which operate intermittently, flight controls must deliver precise, high-force actuation in real time to counter aerodynamic loads, turbulence, and maneuvering demands, making hydraulics the most practical and dependable solution.

Electric actuators have made inroads, but hydraulics still outperform them in terms of force margin and fault tolerance.

Large modern aviation systems are designed with not just one, but multiple independent hydraulic circuits, each with its own pumps (engine-driven, electric, or backup like a Ram Air Turbine [RAT]), precisely because incidents involving partial hydraulic loss do occur, and must be managed without compromising safety.

Of all the pump types included on modern aircraft — fuel pumps, lube and scavenge pumps, air-conditioning and pressurization pumps, water and waste pumps, etc. — hydraulic pumps make up the largest share, well over half of the total pumps installed on an aircraft due to their importance to critical operating functions, further supporting growth projections for the aircraft hydraulic pump market.

Aircraft Types Considered in the Report

The types of aircraft analyzed in Stratview Research’s report include:

- Commercial Aircraft (aka airplanes),

- Military Aircraft,

- Regional Aircraft,

- Business Jets, and

- Helicopters.

How Hydraulic Pump Demand Varies by Aircraft Type

Nearly three-quarters of global aircraft hydraulic pump installations sit on commercial aircraft, and the reason is simple — commercial aviation simply operates at a scale no other segment matches — higher production volumes, higher utilization rates, and far more flight cycles per aircraft.

The global commercial fleet comprises >35,550 aircraft as of June 2025 says the International Air Transport Association (IATA), with Boeing and Airbus collectively accounting for 80% of the current active fleet.

Furthermore, this fleet is predominantly composed of narrowbody jets, reflecting their versatility and lower unit operating costs on most short- and medium-haul routes. As per IATA, the narrowbodies represent about 60% of the total fleet, with two aircraft families, the A320 (including neo variants) and the 737 (including Max) accounting for over 90% of this segment.

This narrowbody-heavy fleet composition has direct implications for aircraft system architectures, particularly hydraulics. In practice, commercial aircraft hydraulic systems operate across two primary pressure classes: 3,000–4,000 psi (207-276 bar) and 5,000 psi (345 bar).

To optimize weight, reliability, and maintenance economics across high-cycle operations, most narrowbody platforms are designed around 3,000–4,000 psi hydraulic systems, a pressure range that has become the industry norm.

Systems utilizing 5,000 psi hydraulic pumps are limited to select widebodies, namely the Airbus A350, A380, and Boeing 787, and a small number of military aircraft and helicopters.

Therefore, the 3,000-4,000 psi systems are expected to compromise the majority of the market share going forward.

This article was written and contributed by Chandana Patnaik, Senior Content Specialist at Stratview Research.

About the Author

Chandana Patnaik

Senior Content Specialist, Stratview Research

Chandana Patnaik is an experienced technical writer, presently serving as a Senior Content Specialist at Stratview Research. She has carved her niche in specific areas including disruptive technologies, information, and specialty chemicals. etc.

She is a regular contributor to various magazines and blogs and writes insightful content that keeps readers stay up-to-date with the latest trends and developments in her areas of expertise.