Global Aircraft Hydraulic Valve Market to Grow 4%

Key Highlights

- Long-term production outlooks for commercial aircraft support future growth potential for the global hydraulic valve market.

- Hydraulic valves used for flight controls will continue to account for the largest portion of market share due to the number of valves required for these systems.

- Continued advancements related to weight reduction and sensor integration will help ensure the longevity of hydraulic valves in the aircraft industry.

Hydraulic systems provide the power density and reliability required for many aircraft operations. A key element of these systems are the hydraulic valves which determine where and when hydraulic power is delivered.

These valves manage the flow of energy across the aircraft’s hydraulic network and direct hydraulic fluid to the right components at the right time to ensure that flight control, braking, and landing systems operate exactly as intended.

Due to the importance of hydraulic valves to the safe operation of aircraft, the continued growth of the global aircraft fleet is expected to drive growth for the valves used in these vessels as well.

Stratview Research is projecting global demand for aircraft hydraulic valves to achieve a compound annual growth rate (CAGR) of 4.20% between 2025 and 2034, pushing annual demand to roughly USD 3.3 billion by 2034.

The research firm anticipates hydraulics valves used for flight control systems as well as those developed for use in commercial aircraft to account for the majority of market share. Meanwhile, advancements in materials and sensor integration will bring new performance capabilities to aid continued use of hydraulics in the aircraft industry.

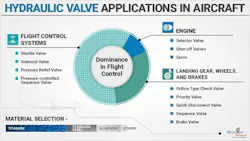

Flight Control Systems to Remain Dominant Application for Hydraulic Valves

Hydraulic valves are distributed throughout aircraft systems, including the engine, landing gear, wheels and brakes, and flight controls.

In 2025, hydraulic valves installed in flight control systems alone accounted for >USD 1.3 billion in value, making this the largest application segment in aircraft valve demand.

Landing gear systems followed, with sales roughly about half of the flight control segment, while engine-related hydraulic valve installations accounted for an even smaller share.

Landing gear and engine components generally operate as simple, intermittent ‘on/off’ or ‘extended/retracted’ systems.

Flight controls, on the other hand, rely on higher pressures, often reaching 3,000-5,000 psi to actuate multiple control surfaces such as ailerons, rudders, flaps, and spoilers, and demand constant, proportional, and high-speed modulation to maintain stable flight.

To ensure precise control of lift, drag, and aircraft stability, these systems require multiple, independent, and redundant hydraulic circuits, which in turn increases the number of valves used.

Commercial Aircraft Will Account for Largest Portion of Hydraulic Valve Demand

Hydraulic valves are used across all aircraft categories, but the highest usage is in commercial aircraft, followed by military aircraft, helicopters, and general aviation/regional aircraft. The difference mainly comes from aircraft size, system complexity, fleet size, and flight-cycle requirements.

Commercial aircraft represent the largest share of hydraulic systems in aviation. Large aircraft have multiple hydraulic circuits, usually two to four systems. These systems operate flight controls, landing gear, brakes, cargo doors, thrust reversers, and steering. A single large commercial aircraft may include 10–15 hydraulic pumps and 20–25 actuators, each requiring valves to regulate fluid flow.

Fleet size also contributes to the commercial aircraft industry dominating market share. Per the International Air Transport Association (IATA), as of August 2025 the global commercial fleet comprises 35,550 aircraft, including 30,300 active units and 5,250 held in storage.

Adding to this, Airbus and Boeing together forecast around 43,000–46,000 new commercial aircraft deliveries globally over the next 20 years (to ~2044). Embraer, the world’s third-largest civil aircraft manufacturer, forecasts ~10,500 new aircraft deliveries by 2044.

These long-term production outlooks help support projections for continued global aircraft hydraulic valve demand in the years ahead.

The commercial aircraft industry also requires frequent maintenance and repair of its hydraulic valves which will aid global demand for these components as well.

The more hours an aircraft flies each year, the more frequently its valves operate, accelerating wear and increasing maintenance, overhaul, and replacement demand. Commercial aircraft typically fly ~10-12 hours per day. This translates to roughly 3,000–4,000 flight hours per aircraft per year depending on airline operations and aircraft type, resulting in increased valve maintenance and replacement demand.

Therefore, both the OEM and aftermarket segments of the commercial aviation sector will continue to create the largest demand for hydraulic valves.

Visit our Market Trends page for more content covering economic and technological trends influencing hydraulic, pneumatic and electromechanical technologies as well as their customer markets.

Titanium Hydraulic Valves Meeting Performance and Weight Reduction Requirements

The bodies of hydraulic valves used in the aircraft industry are made from aerospace alloys chosen for a combination of strength, toughness, and weight. These typically include stainless steel, high-strength aluminum, and titanium.

Even though engineers are experimenting with plastic or composite valves, those made from metal remain the preferred material for high-pressure systems because metals provide better strength, pressure resistance, and reliability.

A substantial share of hydraulic valves used in aircraft today are manufactured from titanium — currently estimated at around half of the total production. Weight reduction remains a dominant design priority for engineers in the aviation industry, and titanium generally sits in the middle between aluminum and steel in terms of density (weight).

Compared to stainless steel and aluminum, titanium offers the advantage of enabling weight reduction without losing durability. Because of this, its adoption is expected to grow further in the future as OEMs continue prioritizing weight reduction as well as durability for their hydraulic valves.

The Future Outlook for Aircraft Hydraulic Valves

The hydraulic valves used in aircraft are steadily evolving into lighter, faster, and electronically integrated components. This is enabling them to remain relevant in the increasingly electrified system architectures being employed in various aircraft.

OEMs are integrating more electro-hydraulic and electro-hydrostatic actuation systems that combine electric control with localized hydraulic power. In the case of the Airbus 380, use of electro-hydrostatic actuation for its flight controls helped to improve the safety of its aircraft.

While this shift in architectures is bringing changes to the design of hydraulic systems on aircraft, it is also offering new development opportunities such as the incorporation of sensors and digital monitoring that will enable continued use of hydraulic valves.

Read the content below to learn more about how recent trade and geopolitical events are impacting fluid power and its customer markets.

Trump Tariffs Causing Uncertainty for Fluid Power Industry

Tariffs Altering Outlook for Industrial and Mobile Machinery Markets

How Global Manufacturing will be Impacted by the U.S.-Iran Conflict

Admittedly, the aviation ecosystem does not operate in a vacuum. Geopolitical tensions, supply chain disruptions, and trade restrictions (see sidebar at right) can occasionally temper production schedules, aircraft deliveries, and component flows across global aerospace networks. Such uncertainties may create short-term volatility in procurement cycles for hydraulic valves and other critical subsystems.

However, viewed from a broader industry perspective, the growth trajectory for the global aircraft hydraulic valve market remains fundamentally positive. As long as aircraft continue to rely on high-force hydraulic actuation systems, hydraulic valves will remain indispensable.

While aircraft architectures advance toward smarter, more electrified platforms, hydraulic valves will continue to adapt — becoming more intelligent, more integrated, and more resilient. And as the global aviation industry scales to meet rising passenger demand and fleet modernization, the hydraulic valve market will, quite naturally, rise alongside it.

This article was written and contributed by Chandana Patnaik, Senior Content Specialist at Stratview Research.

About the Author

Chandana Patnaik

Senior Content Specialist, Stratview Research

Chandana Patnaik is an experienced technical writer, presently serving as a Senior Content Specialist at Stratview Research. She has carved her niche in specific areas including disruptive technologies, information, and specialty chemicals. etc.

She is a regular contributor to various magazines and blogs and writes insightful content that keeps readers stay up-to-date with the latest trends and developments in her areas of expertise.